Fiscal Credibility Meets a Noisy World

A more credible fiscal anchor and easing producer inflation supported domestic assets, even as rising global trade friction, firmer United States inflation and higher oil prices kept external risks elevated.

SOUTH AFRICAN FINANCIAL AND ECONOMIC NEWS

This week’s developments centered on government’s fiscal anchor and tax adjustments, easing producer inflation alongside ongoing cash flow pressures, targeted electricity tariff relief for ferrochrome producers, and an escalating foot and mouth disease response with broader economic implications.

Government Sets Out Fiscal Anchor and Debt Path

National Treasury outlined plans to legislate a principles-based fiscal anchor during 2026, aimed at reinforcing budget discipline and binding future budgets to a transparent debt-stabilisation framework. The proposal is designed to introduce clearer expenditure and borrowing parameters that apply across political cycles, supported by strengthened reporting standards and parliamentary oversight. Over the medium term, the fiscal outlook projects a primary surplus of 0.9% of GDP and a gradual narrowing of the consolidated deficit as spending growth is moderated and revenue collection remains resilient. Gross debt is expected to peak in the near term before edging lower as a share of GDP, signalling a sustained emphasis on credibility, predictability, and containing debt-service costs.

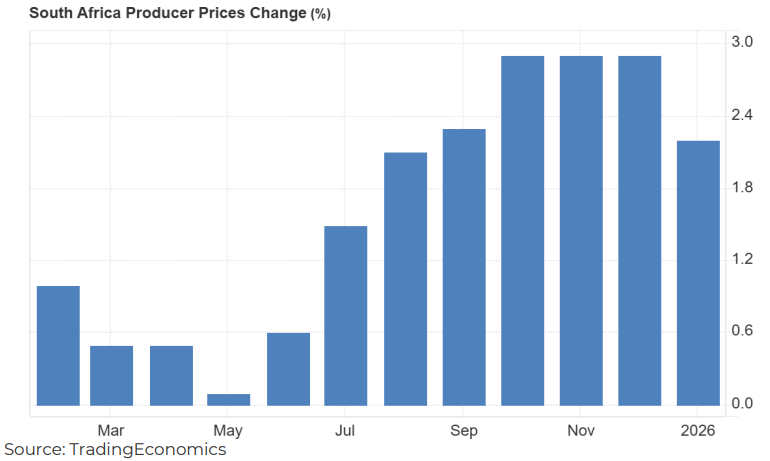

Producer Inflation Eases While Fiscal Pressures Persist

Statistics South Africa reported producer price inflation of 2.2% year-on-year in January, below expectations and driven largely by softer fuel and intermediate goods input costs. The moderation in upstream price pressures suggests limited near-term transmission into consumer inflation. However, broader macro indicators reflected uneven domestic momentum. Money supply growth slowed, private sector credit growth edged higher, and the January trade balance recorded a surplus. At the same time, National Treasury’s January cash position showed a deficit of R69.69 billion, highlighting the uneven revenue cycle and the ongoing strain of financing government operations between peak tax collection periods.

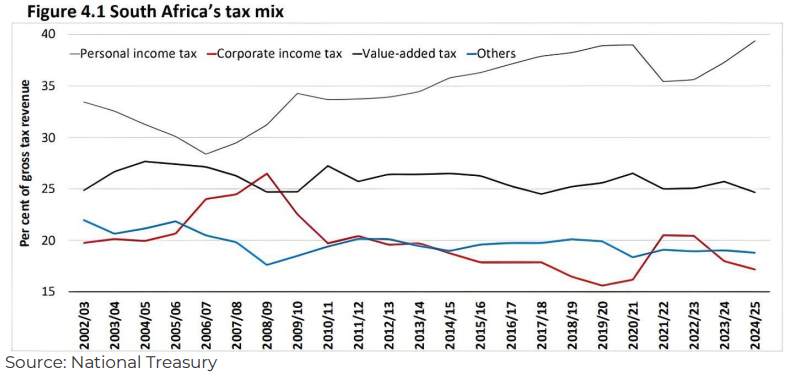

Tax Adjustments Offer Relief as Revenue Surprises on the Upside

Government withdrew the R20 billion tax increase that had been provisionally built into the May 2025 budget, after revising expected gross tax revenue for 2025/26 up by R21.3 billion and lifting the tax-to-GDP ratio to 25.9%. The budget speech attributed the improved in-year outlook mainly to stronger net value-added tax, corporate income tax, and dividends tax receipts, which created scope to avoid additional tax measures without, in government’s framing, undermining fiscal sustainability or near-term economic activity. Personal income tax brackets and medical tax credits were fully adjusted for inflation, reversing two years of partial relief, while a range of thresholds and limits were raised to support small businesses and household saving. The package leans heavily on revenue resilience and compliance gains to absorb spending pressures.

Electricity Tariff Reduction for Ferrochrome Producers

Eskom approved a tariff intervention that cuts electricity prices for Samancor Chrome and the Glencore-Merafe joint venture by 29%, taking the rate to 62 cents per kilowatt-hour. The move is intended to limit retrenchments and support the restart of idled ferrochrome smelting capacity after years of steep power-cost increases. The new rate is below the interim 87.74 cents per kilowatt-hour level set earlier in 2026 and far below the 1.36 rand per kilowatt-hour paid at the end of 2025, improving smelter economics materially. Government indicated the package is initially targeted at the two firms, while a wider industry solution is still being assessed, given that only a small fraction of smelters are currently operating. Terms are still being finalised now.

Foot and Mouth Disease Outbreak Triggers National Response

Government escalated its response to a foot and mouth disease outbreak affecting hundreds of thousands of cattle, declaring KwaZulu-Natal a national disaster area to unlock funding and accelerate vaccination. Import restrictions from trading partners and large-scale culling have disrupted the livestock value chain, raising risks of higher meat prices and export losses. Authorities secured an initial batch of vaccines while indicating substantially more will be required. The episode underscores how agricultural disease outbreaks can quickly translate into broader economic pressures through food inflation and trade channels.

SOUTH AFRICAN FINANCIAL AND ECONOMIC NEWS

23 February – 27 February 2026

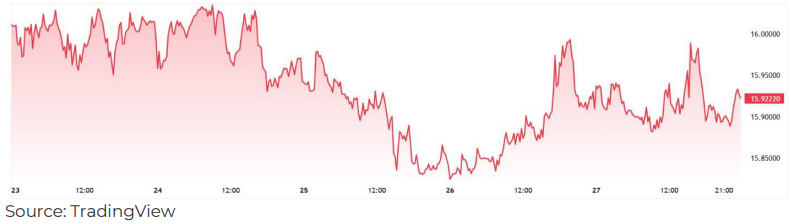

U.S. Dollar / South African Rand [USD/ZAR]

The rand strengthened from R16.01 on Monday’s open to R15.92 on Friday’s close [-0.56%].

The week’s move was mainly about South Africa’s domestic story improving while the United States dollar lacked a clear catalyst. The Budget Speech leaned heavily into fiscal consolidation, including a principles-led fiscal anchor and a projected narrowing in the consolidated deficit, which helped support local bonds and sentiment. That was reinforced by softer producer price inflation, which eased pipeline inflation pressure. In the United States, the dollar was relatively range-bound as markets weighed tariff uncertainty and Middle East risk, and it dipped as Treasury yields fell even after firm producer price data.

Movement: The USD/ZAR closed at R15.92 on Friday, 27 February 2026.

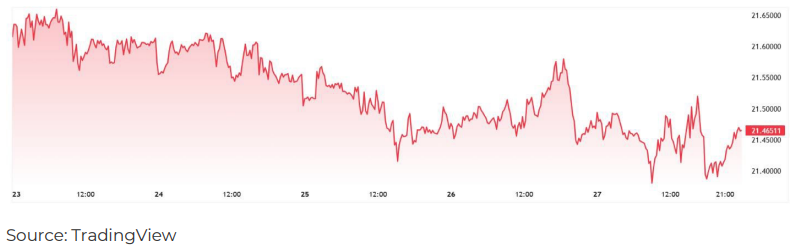

British Pound / South African Rand [GBP/ZAR]

The rand strengthened from R21.61 on Monday’s open to R21.47 on Friday’s close [-0.65%].

Sterling’s side of the equation was shaped by a growing focus on United Kingdom rate cuts, which limited support for the pound. Bank of England messaging kept March easing on the table, even as services inflation remained a watchpoint, and broader UK political and fiscal uncertainty stayed in the background. Against that, South Africa’s budget tone, especially the commitment to a principles-led fiscal anchor, supported the rand’s relative appeal during the week.

Movement: The GBP/ZAR closed at R21.47 on Friday, 27 February 2026.

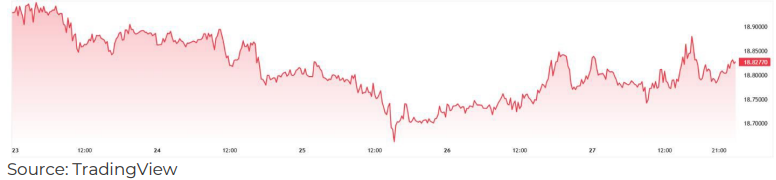

Euro / South African Rand [EUR/ZAR]

The rand strengthened from R18.93 on Monday’s open to R18.83 on Friday’s close [-0.53%].

The euro was influenced by a low-inflation narrative in the euro area, which kept policy expectations anchored and reduced the chance of meaningful yield support for the single currency. The European Central Bank’s consumer survey showed inflation expectations easing, with price pressures seen as contained amid lower energy costs and cheap imports, reinforcing the idea that policy settings can stay steady for now. With South Africa benefiting from a more credible fiscal message in the budget and softer producer price inflation, the relative balance favoured the rand during the week.

Movement: The EUR/ZAR closed at R18.83 on Friday, 27 February 2026.

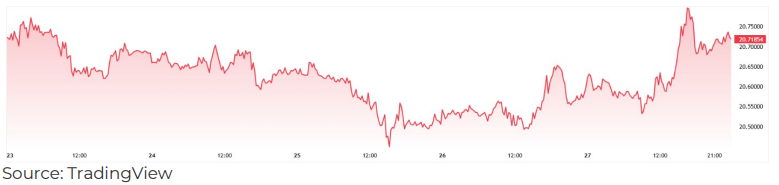

Swiss Franc / South African Rand [CHF/ZAR]

The rand strengthened from R20.73 on Monday’s open to R20.72 on Friday’s close [-0.05%].

Movement: The CHF/ZAR closed at R20.72 on Friday, 27 February 2026.

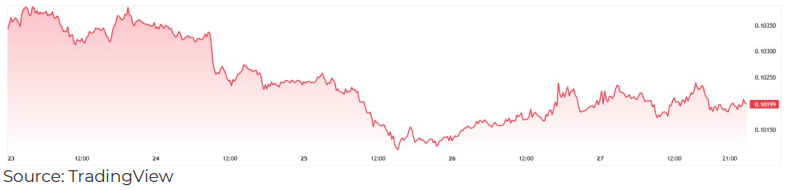

Japanese Yen / South African Rand [JPY/ZAR]

The rand strengthened from R0.1034 on Monday’s open to R0.1020 on Friday’s close [-1.35%].

Movement: The JPY/ZAR closed at R0.1020 on Friday, 27 February 2026.

WEEKLY JSE MOVERS OVER THE PAST 7 DAYS

Overall Market | FTSE/JSE All-Share Index [J203].

The FTSE/JSE All Share Index [J203] rose 4.42% this week, closing at 128,455.68 on Friday after opening at 123,022.00 on Monday.

What Moved the Market

A strong resources-led week, supported by a constructive 2026 Budget signal and softer domestic price pressures, outweighed lingering uncertainty on United States inflation and geopolitics.

- Resources led gains: Gold and platinum shares benefited from firmer precious metals prices amid tariff risk and United States–Iran tension.

- Gold miners added momentum: Solid earnings and shareholder-return updates supported the sector.

- Budget tone improved sentiment: Plans for a fiscal anchor and clearer debt path strengthened the domestic narrative.

- Disinflation aided rate views: Slower producer inflation kept the easing cycle in sight and supported rate-sensitive counters.

- Global rates remained a risk: Hotter United States producer inflation tempered rate-cut expectations.

The week’s advance was primarily a commodities and mining story, with supportive domestic policy optics and easing inflation doing enough to keep the broader tape constructive, even as global rates and geopolitical risks stayed noisy.

Top Gainers

The move appeared to be driven mainly by a continued re-rating of South African platinum equities as platinum group metal prices stayed elevated on tight supply and stronger investor demand, which has increasingly shifted market focus back to near-term cash generation and potential shareholder returns. In Implats’ case, that theme had already been reinforced by its trading update pointing to a sharp interim profit uplift, largely attributed to higher metal prices, keeping attention on the earnings momentum heading into results. Strong sector signals during the week, including upbeat earnings and dividend announcements from peers, likely added to the supportive backdrop for Implats and the broader platinum complex.

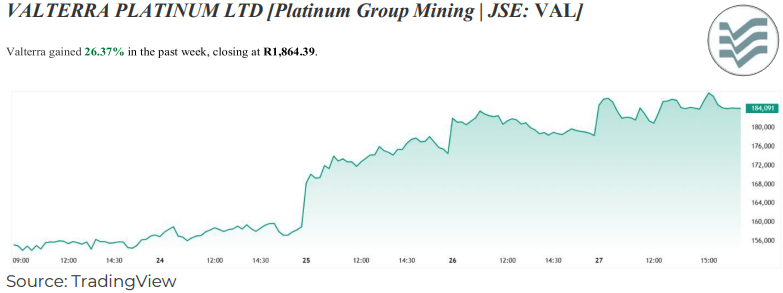

The rally was closely linked to Valterra’s full-year results release and accompanying cash return message: the company reported a sharp rise in earnings supported by higher platinum group metal prices and meaningful cost savings, alongside a sizeable dividend declaration backed by a strengthened balance sheet. The scale of the payout looked to be above prevailing market expectations, reinforcing the idea that the current price environment is translating into distributable cash across the sector. The results landed against a broader platinum market upswing, where record price levels have been underpinned by supply constraints and stronger investment demand, which has further supported sentiment towards the major producers.

Top Losers

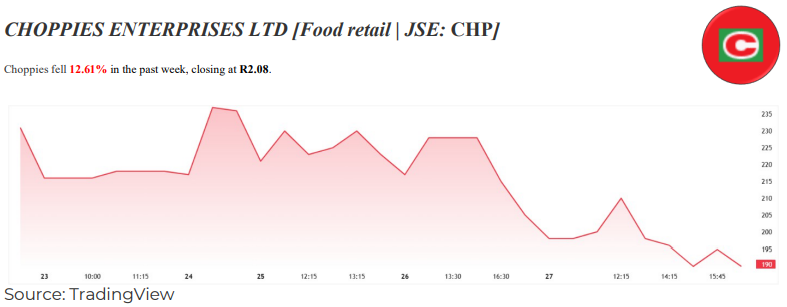

The sell-off largely reflected a one-two hit of leadership uncertainty and margin concerns. The group’s surprise chief executive resignation weighed on sentiment, then a trading update highlighted that heavier promotional activity and an unfavourable sales mix, alongside ongoing investment to recover profitability in KwaZulu-Natal, pressured gross margins in an already intensely competitive food retail environment. Ongoing overhangs from the KwaZulu-Natal SAP disruption also remained in focus, including disclosure of a summons tied to the SAP implementation, which likely reinforced investor caution around execution and residual legal risk.

The decline appeared driven more by liquidity and positioning than by a specific new company announcement. Choppies’ shareholding is unusually concentrated, with a very limited free float, which can make the price highly sensitive to relatively small buy or sell orders and amplify short-term moves on thin volumes. After an exceptionally strong run in 2025 and sharp volatility early in 2026, the continued pullback is consistent with a further unwind of speculative demand and profit-taking in a closely held stock, where sentiment shifts can translate into disproportionate price swings.

KEY INDUSTRY MOVEMENTS

At-a-Glance Takeaways

• ↑ Mining: Higher gold and platinum group metal prices drove strong gains.

• ↑ Financials: Softer inflation and steady bond yields supported sentiment.

• ↓ Food Producers: Profit warnings and margin pressure weighed on the sector.

• ↑ Real Estate: Lower yields offered support, but conviction remained limited.

Mining | FTSE/JSE Mining Index [J177]

The FTSE/JSE Mining Index closed Friday at 183,530.30, up 11.26% from Monday’s open.

Mining outperformed as precious metals strengthened, with gold supported by geopolitical risk and falling United States Treasury yields. Northam Platinum’s strong half-year outcome, including a sharply higher interim dividend, added a clear stock-specific tailwind and reinforced the sector’s earnings leverage to firmer platinum group metal pricing. Policy support also helped at the margin after Eskom cut tariffs for two ferrochrome producers, improving the outlook for energy-intensive smelting. Sentiment stayed risk-on, but the trade remains highly sensitive to any pullback in metals.

Financials | FTSE/JSE SA Financials Index [J580]

The FTSE/JSE SA Financials Index settled at 67,275.53 on Friday, up 1.54% from Monday’s open.

Financials advanced modestly as domestic rates expectations and bond market tone improved around the national budget, keeping hopes of easier monetary policy alive. Softer producer inflation supported the view that price pressures are contained, which tends to help bank funding conditions and valuation multiples. Standard Bank’s successful Flac bond issuance also signalled durable investor demand for local bank credit. The move suggests steady confidence in balance sheet resilience, while investors remain alert to growth and credit-quality risks.

Agriculture | FTSE/JSE Food Producers Index [J357]

The FTSE/JSE Food Producers Index closed Friday at 9,946.35, down 2.69% from Monday’s open.

Food producers lagged on profit caution and competitive pressure. RCL Foods’ trading statement pointing to materially lower interim earnings weighed on confidence, reinforcing concerns about margins in a cost-sensitive consumer environment. Tiger Brands reported volume growth in parts of the portfolio, but highlighted an intensely competitive market that limits pricing power. With inflation easing but demand still uneven, investors appear to be waiting for clearer margin stability before re-rating the sector.

Real Estate | FTSE/JSE All-Property Index [J803]

The FTSE/JSE All-Property Index [J803] closed Friday at 13,034.60, up 0.83% from Monday’s open.

Listed property edged higher as the rates backdrop improved, with budget signalling supporting bond demand and slightly lower long-end yields. That dynamic can ease refinancing pressure for real estate investment trusts and enhance their relative yield appeal. Gains were restrained, however, reflecting ongoing sensitivity to tenant demand, balance sheet discipline and shifts in sovereign yields. The move suggests selective yield-seeking rather than broad-based conviction.

INTERNATIONAL NEWS AFFECTING SOUTH AFRICA

Higher United States tariffs and Middle East tensions lifted trade and oil risks, while firmer United States producer prices, Chinese policy signals amid property weakness, and record global debt pointed to a more fragile global backdrop for South Africa.

United States pushes towards a higher temporary global tariff

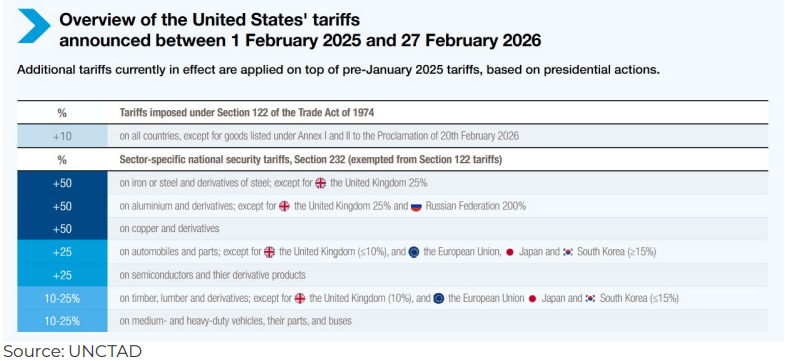

United States trade policy shifted again after a Supreme Court decision curtailed the use of emergency powers for tariffs, prompting the administration to rely on Section 122 of the Trade Act of 1974 to impose a temporary across-the-board import surcharge. A 10% duty began being collected during the week, but officials indicated an intention to lift the rate to 15%, the maximum permitted under Section 122, with the measure set to run for 150 days unless Congress authorises an extension. The order framed the step as a response to a large trade and current-account gap, citing an annual goods deficit of about $1.2 trillion and a current-account deficit near 4% of gross domestic product. The shift has unsettled recently negotiated trade understandings, with major partners seeking confirmation that existing commitments will still be honoured and signalling possible retaliation if the higher rate is applied broadly. Legal debate has also intensified over whether current United States external accounts meet the statute’s balance-of-payments threshold, and industry groups have begun assessing refund claims, with the surcharge estimated to raise roughly $40 billion for the Treasury over the period. For South Africa, a higher blanket United States tariff would raise landed costs for exporters and may further cool global trade and investment demand.

Oil market jolted by Iran tensions ahead of OPEC+ meeting

Oil prices rose during the week after United States and Israeli strikes on Iran heightened concerns about potential supply disruption in the Middle East, with Brent crude trading around $73 per barrel in late-week dealings. At the same time, OPEC+ was reported to be considering a larger-than-expected production increase for April, with options discussed above the previously anticipated incremental adjustment, as key producers weigh market stability against geopolitical risk. The combination of tighter near-term supply fears and uncertain output policy has increased volatility in energy markets. For South Africa, sustained higher crude prices would likely raise fuel and transport costs, with second-round effects on inflation and household consumption.

United States producer prices jump, complicating rate-cut timing

United States producer prices rose more than expected in January, with the producer price index increasing 0.5% month-on-month and 2.9% year-on-year, while core producer prices climbed 0.8% on the month and 3.6% over the year. The data suggest persistent cost pressures in services and trade margins, reinforcing the possibility that the Federal Reserve may keep interest rates elevated for longer than previously anticipated. Market expectations for near-term rate cuts were tempered as investors reassessed the inflation trajectory. For South Africa, a higher-for-longer United States rate environment may keep global bond yields elevated and tighten external financing conditions for emerging markets.

China signals policy support while property market slips again

China’s Politburo called for more proactive and coordinated policies to maintain stability, reiterating support for proactive fiscal policy and a moderately accommodative monetary stance ahead of the March legislative session. The same week, a China Index Academy survey showed new home prices across 100 cities fell 0.04% in February after a January rise, the sharpest monthly decline in more than three years, underlining that the property downturn remains a drag on confidence. For South Africa, softer Chinese construction and household demand can translate into weaker commodity import appetite, affecting export receipts for bulk and precious metals.

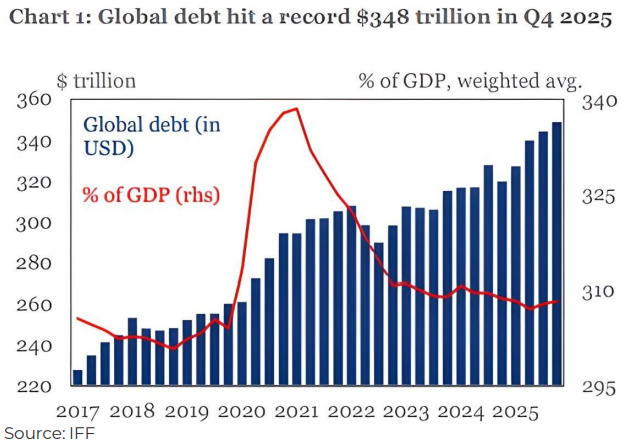

Global debt hits a new record, raising refinancing risk

The Institute of International Finance said global debt rose to a record $348 trillion by the end of 2025, after about $29 trillion was added over the year in the fastest annual build-up since the pandemic surge. The report highlighted heavy government borrowing as a key driver, at a time when interest rates remain high in many major economies and refinancing calendars are becoming more crowded. For South Africa, a more leveraged global backdrop can keep risk premia higher and make it harder for sovereign and corporate borrowers to roll over funding or raise capital for infrastructure and investment.

SOURCES INCLUDED BUT NOT LIMITED TO

This report is published by Everest Wealth for general information and educational purposes only and does not constitute financial advice as defined by the Financial Advisory and Intermediary Services Act, 2002 (FAIS Act). The content is based on market research conducted around the reporting date. Figures and insights may change due to market conditions. Please note that past performance is not indicative of future results. Please consult with a licensed Financial Advisor to determine if such investments are appropriate for your individual circumstances. Everest Wealth Management (Pty) Ltd is an authorised Financial Services Provider (FSP 795) and a registered credit provider NCRCP 21504.